The US Treasury’s ongoing barrage of bill issuance has left market participants trying to gauge when investors will lose their appetite for short-dated government debt.

Buyers have easily soaked up the $1.56 trillion of Treasury bills issued this year through the end of September, with the bulk coming after the government suspended the debt ceiling in June. But drainage of the Federal Reserve’s overnight reverse repurchase agreement facility, where usage has dropped by over $1 trillion as cash is allocated to T-bills, to the widening gap between yields and overnight index swaps — a proxy for monetary policy expectations — are already raising concerns.

ADVERTISEMENT

CONTINUE READING BELOW

“The Treasury’s bill supply increase acknowledges robust structural demand from money market funds and other investors,” said Joseph Abate, a strategist at Barclays Plc. “But how much will this demand grow and, more significantly, how much will bill yields need to cheapen to absorb the additional supply?”

Short-end issuance is being closely watched after the Treasury Borrowing Advisory Committee — a group comprising dealers, investors and other stakeholders — on Wednesday recommended the department skew future issuance toward shorter maturities where liquidity and investor demand is stronger. The committee even supported a meaningful deviation from its historical recommendation of T-bills making up 15% to 20% of all outstanding debt, before a return to the suggested range over time.

Read more: TBAC Advised Skewing Rises to Less Term-Premium Sensitive Tenors

The department is expected to increase bill supply by $700 billion in 2024, with the market growing to 22.4% of outstanding debt from its current share of 20.3%, Barclays estimated in a research note dated Wednesday.

Here’s what to watch for potential signs of indigestion and possible knock-on effects:

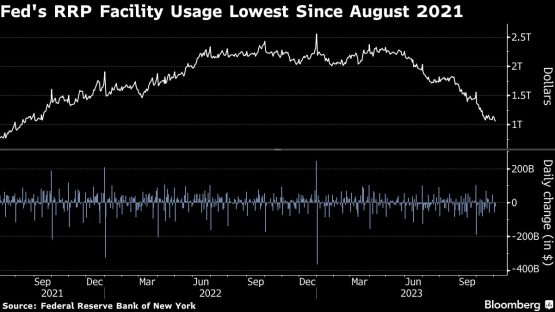

Reverse repo facility

The Fed’s reverse repo facility has been a place where counterparties — mostly money-market mutual funds — can park excess cash to earn a market rate, currently 5.3%.

A combination of liquidity from pandemic-era monetary and fiscal stimulus programs and lack of investable assets like Treasury bills, drove counterparties to stash a record $2.55 trillion there at the end of 2022. Since the supply deluge, usage has dropped to $1.055 trillion, the lowest since August 2021.

Bank of America strategists expect that as balances fall to zero in the second half of 2024 or early 2025, bills could cheapen further and funding pressures will materialize.

Treasury Bill-OIS spread

The spread between the yield on three-month Treasury bills and overnight index swaps has widened since the department unleashed trillions of dollars of supply. The broadening gap suggests that investors are demanding more compensation to buy into the flood of supply.

ADVERTISEMENT

CONTINUE READING BELOW

Since 2001, three-month bills have traded about 9 basis points below OIS — excluding the financial crisis — so by that measure yields are already high, according to Barclays. The firm expects yields to eventually cheapen to 20 basis points or more above OIS, once the reverse repo facility is drained.

Primary dealer holdings

If investors tire of Treasury bills, primary dealers could find themselves sitting on even more short-term government debt.

The more supply that builds up on balance sheets increases the risk that it impedes dealers’ ability to intermediate in other markets, driving up the cost of financing those securities at a time when the US central bank has pledged to keep interest rates higher for longer.

Dealer holdings of bills reached an all-time high $116 billion in July before dropping to $49.5 billion in the week through Oct. 25, New York Fed data show, an indication supply has yet to impair market functioning.

© 2023 Bloomberg