The world’s biggest mining project, a $20bn iron ore, rail and port development in a remote corner of west Africa, is expected to start this year after a 27-year wait beset by setbacks, scandals and several false dawns.

UK-listed Rio Tinto first secured an exploration licence in the Simandou mountains in south-eastern Guinea, 550km from the coastal capital, in 1997. Since then the country of 13mn people has had two coups d’état, four heads of state and three presidential elections.

In that time, Rio Tinto has had six chief executives, lost half the licence, fought drawn-out court battles with several corporate rivals, settled corruption allegations with US authorities and even sought to exit the project completely, only for the sale to fall through.

Finally, in 2024, once Rio Tinto’s state-owned Chinese partners receive the last approval from Beijing, the Anglo-Australian miner intends to fire the starting gun on the most complex project in its history.

“There is nothing else out there of this scale and size,” Rio Tinto’s Bold Baatar told the Financial Times in a recent interview.

Although he is officially head of the copper business, for the past seven years Baatar has been the executive responsible for hauling the project’s complex commercial agreements over the line.

Too expensive for any single miner to develop alone, the project is now a partnership between Rio Tinto, the Guinean government and at least seven other companies, including five from China.

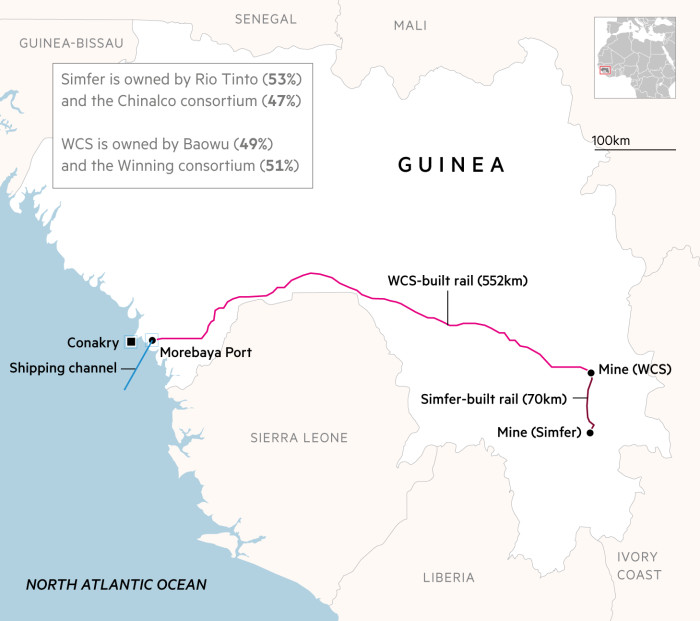

Rio Tinto will build one iron ore mine — known as the Simfer project — in partnership with a consortium led by the world’s largest aluminium producer, Chinalco.

A second mine — known as the WCS project — will be built by Baowu, the world’s biggest steel producer, in partnership with a consortium led by Singapore-based Winning International Group.

At the same time, the parties will co-finance the construction of a 552km railway that will curve through Guinea’s mountainous interior to the sea and the development of a deepwater port on its Atlantic coast.

Rio Tinto and the Chinalco consortium must also fund an additional 70km rail spur to connect its mine with the main line. Rio Tinto’s share of the total cost is forecast to be $6.2bn, more than the company’s entire annual capital expenditure in some of the past five years.

For Baatar, the complex partnership structure at Simandou provides a template for a “new era in co-development” that will be necessary to source the vast volumes of metal required to build the green economy of the future.

One hundred and fifty years of industrial mining mean the simple, easily accessible ore bodies have almost all been developed and complex projects that require ingenuity and large amounts of capital are what is left.

“Historically, when you look at the mining industry, each mine had their own infrastructure,” Baatar said. At Simandou “the capital number is so big for any single party”, he added.

Seven years ago, after a succession of problems, Rio Tinto sought to exit the project, agreeing to sell its stake to Chinalco for up to $1.3bn. Ultimately Beijing, which has to approve foreign investments and divestments by state-owned enterprises, never approved the deal and the project remained on Rio Tinto’s books.

The difference between 2016 and today is that Simandou’s high-grade ore is now even more attractive, given the need to decarbonise steelmaking, according to Baatar.

“The fundamental shift in the last number of years has been that the world is far more in agreement on climate change,” he said.

The steelmaking process, which usually uses coke to produce iron from ore in a blast furnace and then turn it into steel, is highly carbon-intensive, producing about 8 per cent of global carbon emissions.

To cut emissions, the industry is exploring alternative approaches, such as direct reduced iron technology in which the ore is treated using hydrogen and carbon monoxide, rather than coke. Such processes require high-grade iron ore, which is increasingly hard to find in large quantities.

The ore Rio Tinto plans to extract from Simandou has an average iron content of greater than 65 per cent, among the highest in the world. Baatar calls it the “caviar of iron ore”.

Simandou has the potential to help decarbonise the Chinese steel industry, Baatar said.

“A part of the ore body that we’re looking at is very suitable, we think, for direct reduction iron,” he added. “The only way the steelmaking industry globally decarbonises is if China decarbonises.”

China produced 1bn tones of steel in 2022, representing more than half of global production, according to the World Steel Association. The second-largest producer, India, made 154mn tonnes.

Groundworks have already started along the rail corridor and once Beijing approves Chinalco’s investment, Rio Tinto plans to begin mine construction. The first ore is expected to be shipped in 2025, ramping up to full production of 60mn tonnes a year by 2028, representing about 5 per cent of the global seaborne iron ore market.

To add to the complexity, Guinea has been under military rule since 2021 when a junta led by Colonel Mamady Doumbouya ousted Alpha Condé in a coup after the incumbent changed the constitution to run for a third term.

Baatar was unfazed by the politics. “We have been operating in Guinea for over 50 years, through various governments and various forms of governments. There is a strong legacy of institutional memory and commitment to honour the contracts that were set.”

This article has been amended after publication to correct the number of years Rio Tinto has been operating in Guinea