Stocks in Asia fell alongside Europe and US equity futures as investors geared up for a busy week with data due on Chinese activity gauges and the Federal Reserve’s preferred measure of inflation.

MSCI Inc.’s Asia Pacific gauge erased earlier gains as Hong Kong and mainland China stocks slipped. Contracts for Europe and US shares also declined after the S&P 500 rally stalled at the end of last week, weighed by profit taking in megacap tech stocks.

ADVERTISEMENT

CONTINUE READING BELOW

Concerns about China was a focus after 11 Chinese companies lost their credit ratings Friday at Moody’s Investors Service, which withdrew the scores in an unusual flurry that underscores fallout from record defaults. Traders are now waiting if the government will roll out more stimulus after President Xi Jinping on Friday called for a boost in boost the sales of traditional consumer products including cars and home appliances.

Expectations of additional measures were also fueled by weak borrowing by local governments, stirring speculations that Beijing may pick up their slack and take on more debt. Whether or not existing stimulus bodes well for the economy will be scrutinised when China publishes purchasing managers’ data later this week.

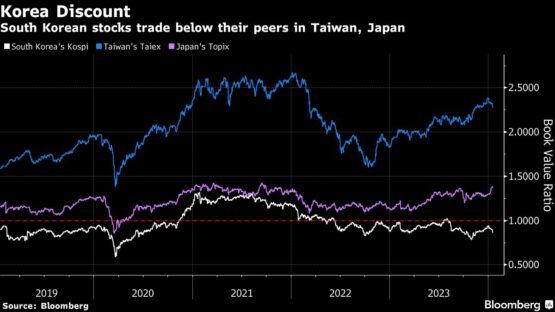

In South Korea, stocks trimmed their losses after declining as much 1.4% on the authority’s plan to push listed companies to improve management and corporate governance, which some investors found as lacking details.

“The disappointment comes from the fact that companies are not required to take any actions in the short term,” said Seol Yongjin, an analyst at SK Securities Co. “Investors expected specific incentives to be announced today but now the government said those details will be disclosed later this year.”

Japanese equities were outperformers as both the Tokyo Stock Price Index and the Nikkei-225 Stock Average gained, with the latter extending record highs. Japan trading house stocks rose after Warren Buffett said in his annual shareholder letter that the companies follow investor-friendly policies that are “much superior” to firms in the US.

Elsewhere, New Zealand’s dollar fell against all Group-of-10 currencies as traders weighed the nation’s monetary policy outlook. Treasuries extended gains in Asia, while Australian 10-year yields dropped nine basis points.

Eyes on PCE deflator

This week, investors will be bracing for the impact from heavy Treasury and corporate issuance and month-end positioning. There’s also a slate of economic data to be sifted through, including the so-called core personal consumption expenditures price index on Thursday – the Fed’s favored inflation gauge.

Headline and core PCE are both set to come in at a hot 0.4% month-over-month pace — versus 0.2% prior for both — driven in large part by residual seasonality, according to Bloomberg Economics.

ADVERTISEMENT

CONTINUE READING BELOW

“Despite the high monthly reading, base effects will likely allow annual core inflation to edge down to 2.8% in January (vs. 2.9% prior) and continue to fall to 2.5% or lower by mid-year, supporting our baseline expectation for a first Fed rate cut in May,” Tom Orlik, chief economist, wrote in a note.

Federal Reserve Bank of New York President John Williams said in an interview published Friday that the economy is headed in the right direction, and it will likely be appropriate to cut rates later this year. A slew of Fed speakers this week are likely to reiterate William’s comments that the central bank doesn’t feel pressure to begin cutting rates anytime soon.

In commodities, oil followed a weekly drop with further losses as traders awaited fresh clues about global demand and balances in March and beyond. Gold was slightly down while iron ore fell to the lowest since October — after dropping almost 9% last week — with hopes for a rebound in Chinese steel demand following the Lunar New Year holidays fading.

Key events this week:

- Japan CPI, Tuesday

- Bank of England Governor Andrew Bailey speaks, Tuesday

- US Conf. Board consumer confidence, durable goods, Tuesday

- Reserve Bank of New Zealand rate decision, Wednesday

- Eurozone economic, consumer confidence, Wednesday

- FTSE 100 index review, Wednesday

- US GDP, Wednesday

- Atlanta Fed President Raphael Bostic, Boston Fed President Susan Collins, New York Fed John Williams speak, Wednesday

- G-20 finance ministers and central bank chiefs meet, Wednesday

- Australia retail sales, Thursday

- France, Germany and Spain CPI, Thursday

- US PCE Deflator, Thursday

- Chicago Fed President Austan Goolsbee, Atlanta Fed President Raphael Bostic, Cleveland Fed President Loretta Mester speak, Thursday

- MSCI index changes, including the removal of 66 Chinese firms from the MSCI China Index, come into effect at the close, Thursday

- China official PMI, Caixin manufacturing PMI, Friday

- Eurozone CPI, Friday

- US ISM Manufacturing, University of Michigan consumer sentiment, Friday

- US House funding bill deadline to avert a government shutdown, Friday

- Atlanta Fed President Raphael Bostic, San Francisco Fed President Mary Daly speak

Some of the main moves in markets:

Stocks

- S&P 500 futures fell 0.2% as of 2:18 p.m. Tokyo time

- Nikkei 225 futures (OSE) rose 0.3%

- Japan’s Topix rose 0.6%

- Australia’s S&P/ASX 200 rose 0.1%

- Hong Kong’s Hang Seng fell 0.5%

- The Shanghai Composite fell 0.3%

- Euro Stoxx 50 futures fell 0.3%

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro was little changed at $1.0820

- The Japanese yen was little changed at 150.43 per dollar

- The offshore yuan was little changed at 7.2040 per dollar

- The Australian dollar fell 0.1% to $0.6555

- The British pound was little changed at $1.2666

Cryptocurrencies

- Bitcoin fell 0.5% to $51,516.5

- Ether fell 0.2% to $3,103.26

Bonds

- The yield on 10-year Treasuries declined two basis points to 4.23%

- Japan’s 10-year yield declined three basis points to 0.685%

- Australia’s 10-year yield declined 10 basis points to 4.09%

Commodities

- West Texas Intermediate crude fell 0.5% to $76.14 a barrel

- Spot gold fell 0.1% to $2 033.10 an ounce

This story was produced with the assistance of Bloomberg Automation.

© 2024 Bloomberg