In 2023, standards became higher than ever for global tech. Customers want to be able to buy something in two clicks but still need in-person customer service. Workers want to work digitally, ideally from a beach somewhere, while maintaining a connection with their colleagues. And the truth is these standards are unlikely to get lower soon.

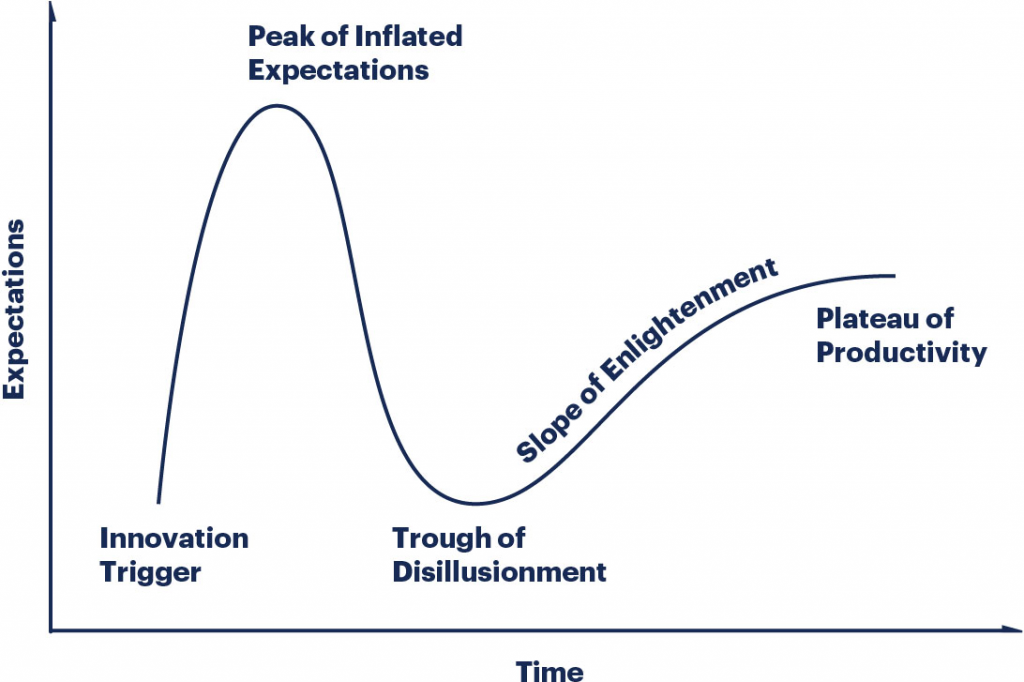

In Africa, the tech scene hasn’t been any less dramatic. It was, in many ways, a market correction. Several startups shut down, while many others survived by bone-deep cost-cutting or mergers and acquisitions. Founders and investors have gone from chasing Silicon Valley-esque growth to seeking a balance with the African market. Between 2020 and 2023, African tech went from the “peak of inflated expectations” point to the “plateau of productivity” side of Gartner’s hype cycle.

Now, what’s next? That’s what everyone wants to know as we enter a new year. Predicting the future is hard and risky. But it’s even harder in the digital tech industry because, as we’ve seen in the past three years, things change fast and dramatically. However, 2023 gave several pointers to trends we should all pay attention to in the new year.

Crypto/Web3

2022 was a rough year for the crypto market. Everything went wrong, from Terra’s downfall to FTX’s scandal. But 2023 was a lot better as Bitcoin ended the year over 150% higher than where it started. The Solana blockchain also made a dramatic comeback, with its token rising over 1000%.

Why does this matter? Because price is still the main driver of the crypto ecosystem. Funding pours into startups when prices are high and dry up when prices are low. It also means the hype bubble will likely return because markets become irrational in the face of high prices.

Africa is the fastest-growing cryptocurrency market among developing economies, primarily because people seek to hedge against inflation. Young people are drawn to low-barrier opportunities to generate wealth, which is crypto’s biggest use case today.

Africa’s regulatory environment is also slowly buying into crypto. In December, Nigeria’s central bank lifted a ban on cryptocurrency transactions, saying global trends had shown a need to regulate such activities.

Artificial intelligence

AI has become the rave of the moment, thanks to OpenAI’s breakthrough with ChatGPT. The chances that an image or text you see on social media are products of generative AI are higher than ever. Every big tech player is in the race for AI dominance. Google launched Gemini in December, a few weeks after Elon Musk’s xAI launched Grok, another ChatGPT competitor.

One in every four dollars that went into the pocket of an American startup was related to AI, per Crunchbase data. According to McKinsey data, AI startups garnered over five times as much funding in the first half of 2023 as they did over the same period in 2022. Global demand for talent in this section also spiked in 2023. LinkedIn job postings that mention AI or generative AI have more than doubled since 2021.

In Africa, we are seeing more startups either focus on AI or apply it to their processes. For instance, OnePipe, a Nigerian fintech, uses artificial intelligence for fraud detection and prevention and biometric verification for customer KYC implementation. It also uses natural language processing for conversational transactions. Nokwary, a Ghanaian startup, uses speech recognition and conversational user interfaces to enable visually impaired people and those who can’t read and write to interact with banking apps and systems through spoken commands.

The biggest challenge to an AI boom in Africa is data. However, this poses a huge opportunity for research and data collection companies in the continent.

Mergers and Acquisitions

Many startups shut down between 2022 and 2023, either because they couldn’t raise more cash or because tough economic times got the better of them. But that wasn’t the only trend that emerged. Many others survive by getting acquired. Nearly 70 acquisitions have happened between 2022 and 2023, according to data from The Big Deal and BD Funding Tracker. Some notable deals were Risevest and Chaka, BioNTech and InstaDeep, Bitmama and PayDay, and FairMoney and PayForce.

Mergers and Acquisitions will likely remain a trend for as long as valuations are low. Over the last two years, startups have been more cautious about bloating their valuations, and investors have kept the same sentiment. It’s partially why we haven’t recorded new unicorns in a minute. MNT-Halan was the only new entrant in the last two years.

This also creates an opportunity for African startup marketplaces, which will replicate Acquire.com to make acquisition easy for startups with solid products but low clout.

International work for Africans

Many African countries saw their currencies devalued in 2023. Inflation rates have also spiked in many economies. This creates a stronger appeal for them to earn foreign currencies and an [almost worrisome] opening for Westerners to find cheap labour in Africa. This is crucial because wage rates are rising in China and India, making it increasingly expensive for companies to outsource services there.

Studies by Bloomberg show that China’s upper-middle class now dominates, with over 200 million urban households having disposable incomes of $16k — $34k. Meanwhile, many Sub-Saharan economies have seen their middle-class shrink in recent years.

Also, there aren’t enough opportunities for young people to work remotely in Africa. Ten to twelve million young Africans enter the labour market each year, and an estimated one-third of the 600 million young people entering the global market by 2030 will be young Africans.

This trend will create opportunities for new approaches to apprenticeship or employment matching. It also means startups focused on building tech talent will likely see growth in 2024.

New regional preferences

In 2024, investors could reevaluate their regional strategies in response to changing macroeconomic and political conditions. Per the EIU, fifteen African countries have elections next year, and investors will observe their outcomes keenly. Elections are fraught with risk, especially in regions where armed conflict is rampant. The EIU notes that elections in Algeria, Egypt, Ghana, and South Africa will add to political risk, which could have long-term implications on where investors put their money.

An AVCA survey revealed that LPs favoured investing in West Africa while GPs leaned towards East Africa. The data aligns with this: between 2019 and 2023, per The Big Deal, there were over 700 recorded deals worth $1m or more. West Africa led the pack with 246, East Africa with 175, Northern Africa with 160, Southern Africa with 147, and Central Africa with 14. Depending on the degree of confidence, the numbers could realign with investors becoming more risk-averse. It’s all “wait and see” going into 2024.